Adapted from article by Thenesh Kannaa, AT-mia.my

1 January 2019 didn’t just mark the first day of 2019, but also the requirement for Malaysian businesses to self-account for 6% service tax upon procuring certain services from foreign service providers. This requirement applies even to Malaysian businesses that are not service tax registered.

Why this new requirement?

2018 was a year of unprecedented changes for Malaysia vis-à-vis the political front as well as taxation, particularly indirect taxation. Goods and Services Tax (GST) was reduced to zero per cent effective 1 June 2018 and formally repealed effective 1 September 2018.

Following the three-month tax holiday period, Sales Tax and Service Tax (SST) was implemented effective 1 September 2018.

One of the key differences between GST and SST is that SST is a single-stage taxation, which means that businesses that incur SST on their acquisition are generally not eligible for a credit of the SST incurred on their costs/acquisitions.

As a result, businesses would prefer to acquire goods and services without SST to keep the costs low (there’s no compelling reason for such preference in the GST regime given that businesses are generally granted an input tax credit in respect of any GST incurred on acquisition).

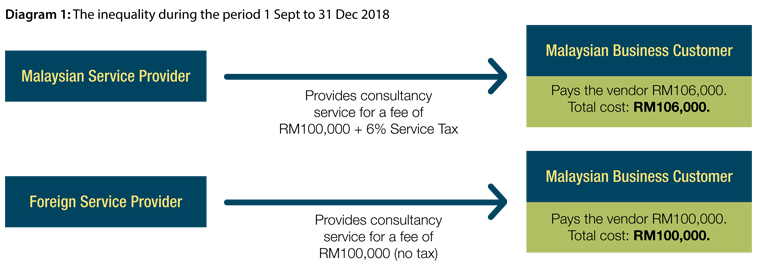

Hence, during the period 1 September 2018 to 31 December 2018, Malaysian service providers were arguably at a disadvantage as they had to charge 6% service tax to their customers on provision of taxable services. However, these customers would not incur any service tax if they had purchased the same service from a foreign provider. This inequality is illustrated in Diagram 1 below.

As illustrated in Diagram 1, the Malaysian service provider is required to charge 6% service tax but the foreign service provider, which does not have any establishment in Malaysia, is not required to charge service tax.

Given that no input tax credit is available under the SST regime, the Malaysian business customer would prefer to acquire the services from a foreign service provider. To avoid such bias and any potential serious consequences in the long run, the imported services tax was introduced effective 1 January 2019.

The concept of imported services tax

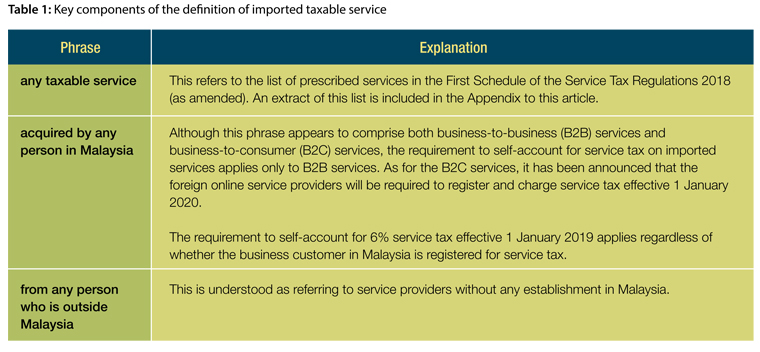

Imported taxable service is defined in the Service Tax Act 2018 (as amended) as any taxable service acquired by any person in Malaysia from any person who is outside Malaysia. The three key phrases in the definition are further explained in Table 1 below.

The reverse charge mechanism during the GST era were limited to situations where the services are consumed in Malaysia. There’s no express provision that limits application of imported service tax based on place of consumption. However, Customs has recently expressed its interpretation that accommodation in a hotel overseas is not an imported service, and hence not subject to imported service tax. No detailed reasoning was offered to support the interpretation and hence the criteria used by Customs to determine whether or not a service is being “imported” is yet to be known.

Continue reading: https://www.at-mia.my/2019/02/15/procuring-service-from-foreign-providers-heres-an-additional-6-tax/